“We’re too small for a self-insured health plan”

“We’re too small for a self-insured health plan”

When speaking with employers about their company health plan it’s common to hear statements like “I know we could benefit from a self-insured health plan, but we are too small for self-insurance.”

Although this is a fair statement and has historically been true, the adoption and success of captive health plans is making self-insured health plans a possibility for more employers.

Captive insurance plans have been used in the Property & Casualty space for a long time and have more recently been utilized within the health insurance markets.

Captive health plans provide a vehicle for employers with less than 500 employees to reap the financial benefits and customizability of self-insured health plans, which under normal circumstances would be far too risky to implement.

So what makes captive health plans worth exploring?

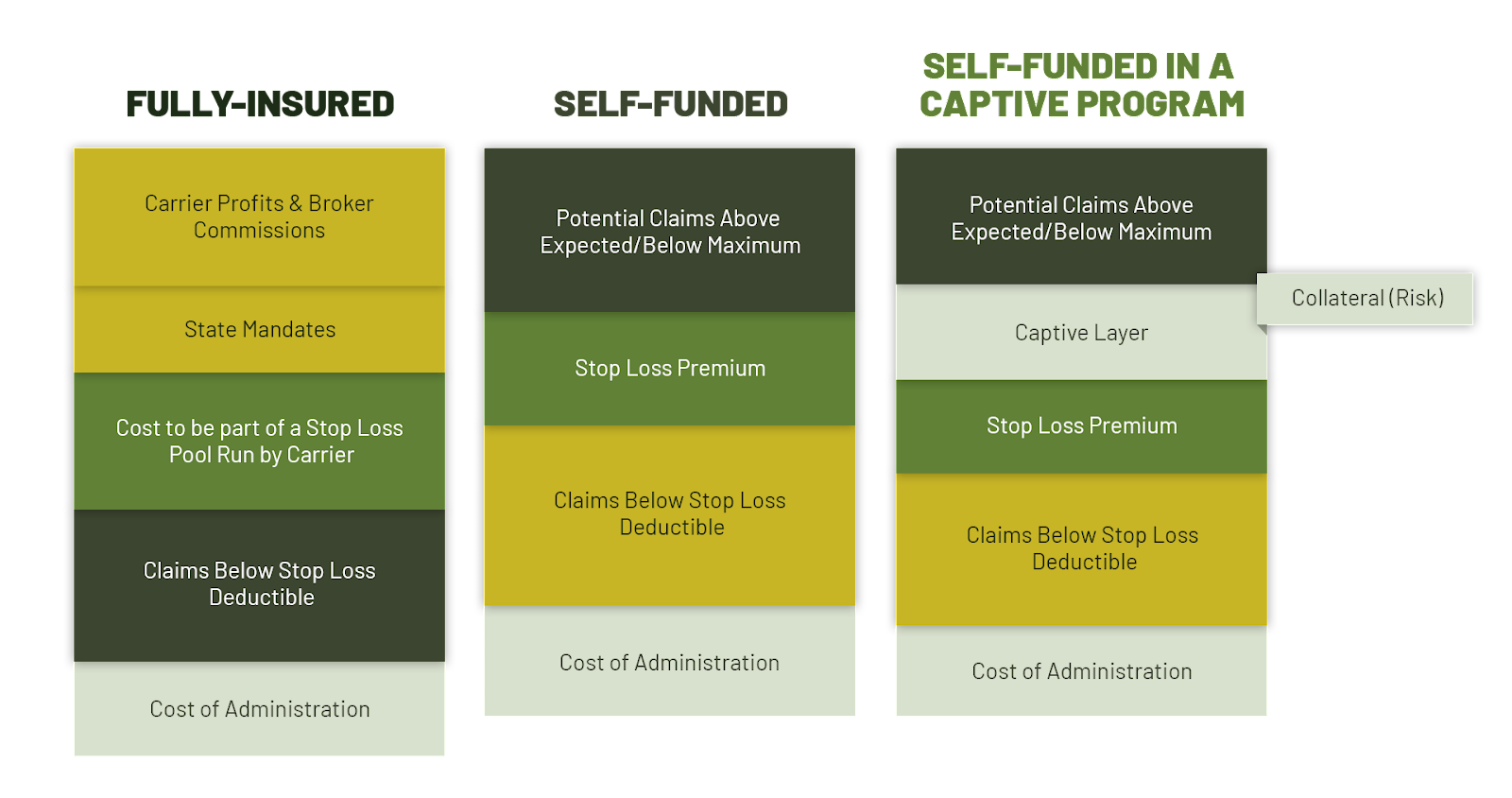

Transparency of healthcare costs

Fully-insured health plans allow for limited access to a customer’s claims data or the underlying costs of the plan. Typically you only see your monthly premium costs and getting claims data is like pulling teeth.

Captive health plans allow for the transparency of traditional self-funded health plans with an added layer of protection.

Access to your claims data.

Ability to select the vendors who supply healthcare services to your employees and negotiate with them on price.

Reduced taxes and admin costs.

Excess premiums (or profits) are realized and returned to the members of the captive. More on this later.

Greater predictability

The captive pooling structure helps reduce volatility and mitigate risk exposure.

Increasing the size of any population results in greater predictability of future risks and this can be leveraged by captive health plans. An employer with 100 employees is considerably less “predictable” as compared to a captive population of 1,000 or even 10,000 employees.

Also, the captive serves as an additional layer (buffer) between the self-insured employer and the stop-loss carrier, since the risk associated with high-cost claims can be spread across the members of the captive. The risk within this captive layer is shared by a cohesive group of employers rather than the Wild West of the general insurance pooling.

Reap the rewards of better claims management

The captive allows for the accrual of excess premiums accrued by the group to be paid back as dividends, rather than those dollars being retained as profits by the stop loss carrier or health plan administrator.

It’s clear who has been realizing and retaining profits of Fully-insured health plans…

Since there are real dollars on the line (dividends), members of the captive have “skin in the game” – an incentive to implement the necessary solutions to control the costs of high claims.

Risks to captive health plans

As a member of a captive you won’t have much control over what employers enter or exit the captive. This means an employer may enter the captive who consistently sees high claims and those employers with healthier employee populations will be subsidizing the costs.

But these risks must be weighed with the alternative risks of implementing a traditional self-insured health plan (high volatility, low predictability) or purchasing a fully-insured health plan (low transparency, guaranteed premium increases).

Is a captive health plan right for you?

Captive health plans are not for every employer, but if you are interested in the transparency and financial benefits of self-insured health plans and want greater control over the healthcare your employees have access to they are worth exploring.

Sources: